Here's what you need to know about giving and receiving gift funds.

Saving a down payment is one of the most challenging—aspects of buying a home. The larger your down payment, the less you have to finance, which can lead to lower interest rates and monthly payments over the life of your loan. Furthermore, with a 20% down payment or more can help you avoid costly private mortgage insurance.

If you're ready to become a homeowner, asking your family for help with your down payment may have crossed your mind. While down-payment funds can be gifted between family members, you must follow a list of rules to document the gift, including a down payment gift letter.

If you’re lucky enough to get down-payment help this year (or generous enough to give it), be sure you know the rules around gift funds. It’s not as simple as handing over a wad of cash with a note that says “Congrats! Here’s a little something for your new house.”

Down payment gift funds must meet certain requirements or the gift giver and recipient face trouble down the road. From writing a gift letter to rules around repaying gift money, here are basic facts homebuyers and donors should know.

Who can gift a house down payment?

It might seem odd that there are restrictions around who can give someone money for a down payment. After all, money is money, right? Not necessarily. Cash can come with strings attached, which might affect the borrower’s ability to repay the mortgage.

How much money can you receive as a gift?

Many home loan programs allow some or all of a down payment gift to come from a variety of sources. You can get gift money from a relative, friend, your employer, local labor union, government agency or even a charitable organization.

The amount of gift funds you can apply to your down payment depends on what loan program you select. Here’s a look at the most common options.

Fannie Mae gift funds.

Fannie Mae guidelines allow approved lenders to offer conventional loans, the most common type of home loan taken out in the U.S. The minimum down payment for a conventional loan is 3%, and the entire amount can come from a gift for a one-unit primary residence. A 5% minimum down payment from your own funds is required if you’re buying a two- to four-unit property.

Freddie Mac gift funds.

Similar to Fannie Mae, Freddie Mac provides funding for conventional loans. Under Freddie Mac guidelines, your entire down payment can be gifted by a relative if you’re buying a single-family home as your primary residence. You’ll need to come up with up to 3% of your own down payment funds if you’re purchasing a two- to four-unit property with less than 20% down.

FHA gift funds.

The Federal Housing Administration (FHA) insures loans made by FHA-approved lenders and allows the entire 3.5% down payment to be gifted. An FHA gift letter paper trail is required, with supporting documents resembling conventional guidelines. FHA loans, which have lower credit score requirements and a low down payment requirement, can help first-time homebuyers who need more flexible borrowing guidelines.

VA gift funds.

The Department of Veterans Affairs (VA) guarantees home loans for eligible active and retired military borrowers. VA loans do not require a down payment, but the program does allow borrowers to use gift funds toward a down payment if they want to make one. The gift letter and documentation requirements are similar to FHA and conventional loans.

USDA gift funds.

Families with low- to moderate-incomes can purchase homes in rural areas of the U.S. using the U.S. Department of Agriculture’s mortgage program. Like the VA loan program, USDA loans require no money down. Gift funds are permitted with a properly completed down payment gift letter and supporting documents consistent with FHA, VA and conventional lending rules for gift letters.How Does Using Gift Money for a Down Payment Work?

You can use gifted funds to make a down payment, but the mortgage lender will want to know some details before they allow you to use it. Only two specific groups can give a home buyer money to fund their down payment.

- A family member — as long as they can prove they have a standing relationship with the buyer

- Government organization — as part of a program meant to get first-time buyers into the market

You must confirm the relationship between you and the gift giver.

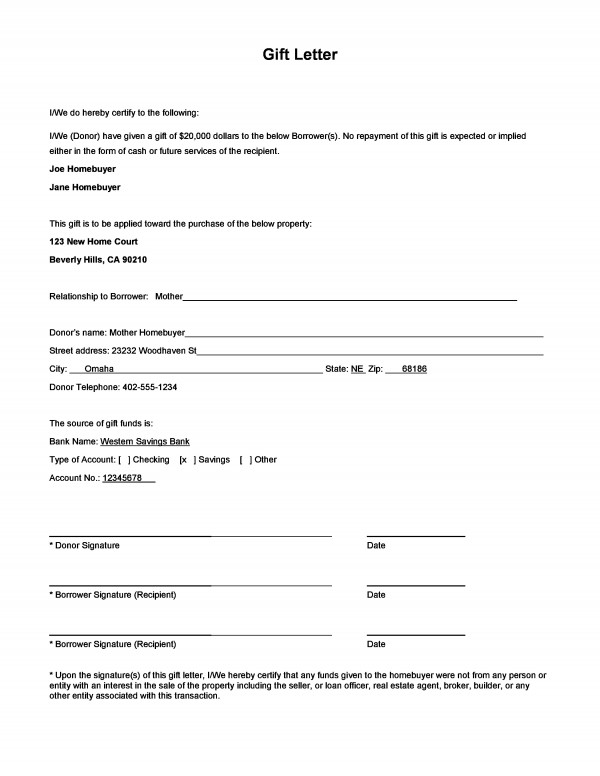

If you plan on getting gift funds from a family member, you’ll need a letter that confirms your relationship and that the money is a gift and not expected to be repaid. Usually this is in the form of a gift letter, which both parties sign. Your lender will provide the required format.

Sample Gift Letter

The lender will also require further evidence of the gift — for instance, they will ask to see the donor's bank statements to show they have the funds to give the buyer as much money as is promised. They may also ask for a bank slip from the buyer’s account to show when the money was transferred, and a bank statement from the borrower after the money is deposited.

Often, gifts change hands during the application process — this gives time for the money to show up on both the donor and the buyer’s bank statements as well as gives the mortgage lender time to verify that the money is from a legitimate source and the pair has an appropriate relationship.

If the gift funds are added to the buyer’s bank account after settlement, then documentation will still be required before it can be applied to the purchase. Typically, this will require a receipt of the cashier’s check as given to the closing agent.

Can you pay back a mortgage gift?

The answer is NO. This is considered mortgage loan fraud, which is a crime. It can also put your loan qualification at risk as all loans need to be factored into your debt-to-income ratio.

The moral of this story: Be honest with your lender about where you’re receiving all funds for your down payment — as they’ll likely find out anyway.

What Else Should You Know About Down Payment Gifts?

As previously mentioned, there’s a difference between receiving a down payment gift and a loan. Buyers need to be clear with their mortgage lenders and confirm that the money received was gifted. A sudden infusion of cash without a traceable source will leave lenders suspicious and, perhaps, wary of completing the loan deal on their end.

Buying a Home is More Than a Down Payment

Ultimately, the cost of the down payment is only one expense to consider in the home-buying process. Homebuyers need to pay for closing costs, which include expenses like an appraisal, credit report, and underwriting fees.

The Do’s and Don’ts of a Down Payment Gift

| Do… | Don’t… |

| Get a signed statement from the gift giver | Tell the lender the funds are a gift when it’s a loan |

| Remind gift giver to keep a paper trail | Change or add money without explanation |

| Get the money in advance and know how seasoned money works | Assume all loan types allow down payment gifts |

| Understand the monetary limit of gift funds for tax purposes | Neglect the mortgage because you have no money in the game |

Down payment gifts can make it easier for homebuyers to afford a home.

If you’re in the market for a new home and want a little help, don’t hesitate — just make sure you follow the above steps to ensure you accept such a gift in the proper manner. When you speak with your lender about what loan is best for you, make sure you let them know upfront that you plan on using gift funds for the down payment. Some loans have strict guidelines on how much gift money you can use for a down payment and who can gift you the money.

Reach out of you have questions or need help!

CMG Financial | NMLS 1820

8337 W. Sunset Road, Suite 300

Las Vegas, NV 89113

Office (702) 777-1306

Aundrea Beach-Greco

Mortgage Advisor, CMPS

NMLS 333739

(702) 326-7866

info@aundreabeach.com

www.AundreaBeach.com